Just over three months ago, financial markets started responding to the news of a new pandemic. Within the following four weeks S&P 500 fluctuated between 3,373 and 2,237, effectively losing a third of its value. One of the most significant financial valuation melt-downs was on its way.

By the end of May, most economic measures were pointing to a significant decline, yet the financial markets surprised many observers with a swift recovery. NASDAQ was trading above its 2019 levels, while S&P 500 was back above 3,000. Yet, the small stock Russell 2000 index remained under its December levels, thus suggesting a greater impact the pandemic had on smaller public companies.

Valuations were impacted by both new systemic risks and companies’ individual exposure to the crisis. Market multiples, financial forecasts, and discount rates were all conduits between the current state of economy and financial valuations.

Market Multiples

Stock markets can inform the valuation of a specific company through so-called market approach. Guideline public companies supply market multiples, which help to convert the company’s financials into valuation estimates.

Valuation = Market Multiple * Financial Measure

In our recent valuations, we found that both market multiples and financial measures were impacted by the onset of Covid-19 pandemic.

For one of our SaaS software clients, a forward-looking revenue multiple dropped from 5.3x to 3.3x between July 2019 and March 2020. For another media tech company, EBITDA multiple remained steady at around 4.3x – 4.5x between December 2019 and April 2020.

Companies were making material adjustments to their 2020 budgets and long-range forecasts, which were used against 2020 and 2021 market multiples. In many valuations, declines in market multiples were exacerbated by lower forecasts, thus leading to substantial drops in value, and potentially explaining why smaller companies devalued more than their larger peers.

Discount Rates

Discount rates are used in a so-called income approach where the value of a company is a total of discounted future cash flows.

Unlike market multiples, discount rates are not directly observable. Deriving one requires careful calculations, a ton of data, and a bucket-full of subjective judgement. Falling market multiples imply greater cost of capital, directionally, but exceedingly hard to convert into exact numerical estimates.

Due to the high level of subjectivity around discount rates, a perceived aggressiveness of the financial forecast is a factor when calculating one. We found that many private companies decreased their forecasts sufficient to keep most of the discount rates unchanged from those used in 2019. In other situations projections came so low that we had to adjust other assumptions in the DCF model to arrive at meaningful conclusions. Meaningful conclusion often meant those inline with the market approach.

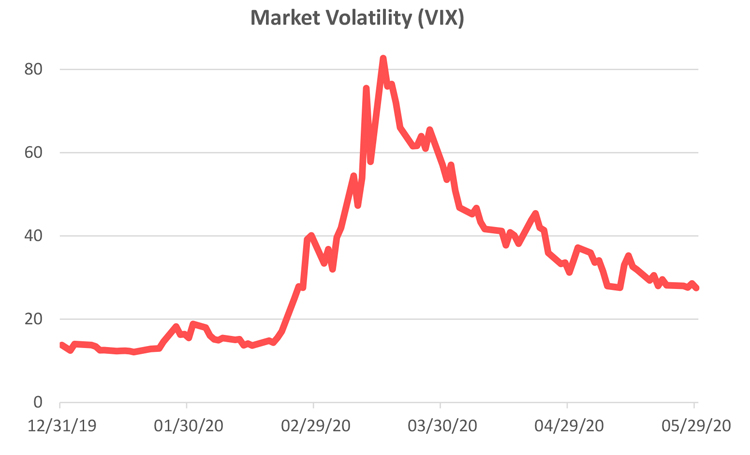

Market Volatility

Valuations of derivative financial instruments, securities within complex capital structures, contingencies, and earn-outs are all heavily influenced by the volatility of an underlying instrument(s).

Broadly speaking, VIX, over-the-counter index tracking volatility, finished 2019 at 13.78, spiked around mid-March to 82.69, and subsided to 27.51 by the end of May. Within a specific sector, volatility can be measured from a set of publicly traded peers. In our recent experience, the groups of publicly traded peers diverged as some registered increased volatility, while for others volatility had declined from its pre-covid-19 levels.

As with market multiples, discount rates, or financial forecasts, volatility estimates can be very subjective. However, once the method and the peer-group are set, updated volatility models produce very deterministic results.

While higher volatility may increase the value of a derivative instrument, the value of an underlying asset remains the major factor. In our recent work, we often found that an asset value had a stronger impact on the value of the derivative than that of the increased volatility.

Conclusion

As expected, Covid-19 had a material impact on financial valuations. Most business valuations decreased, but not without notable exceptions. About every part of the business valuation analysis was affected by new market data and company-specific financial outlook.

Market multiples offered the most direct indication of how much values have changed, the result that was often amplified by a private company’s own circumstances. Financial derivative values were helped with often higher volatilities, however, a lower value of an underlying asset had a stronger effect on value.

As a result, the current environment makes it nearly impossible and certainly not prudent to make any assumptions about values of things without running careful calculations first. Based on our recent experience, the situation of high uncertainty is still here, and may continue until we see key economic measures begin to stabilize.